New York City is renowned for its vibrant economy, bustling streets, and diverse population. However, living or doing business in the Big Apple comes with its own set of financial responsibilities, particularly when it comes to NYC state tax. Whether you're a resident, a small business owner, or a corporate executive, understanding the intricacies of New York's taxation system is crucial to ensuring compliance and optimizing your financial health. In this article, we'll delve deep into the world of NYC state tax, breaking down the key components, offering practical advice, and providing actionable insights to help you navigate this complex terrain.

From income tax to sales tax, property tax, and more, New York City imposes a variety of levies that contribute to the state's revenue stream. These taxes fund essential services such as public education, healthcare, infrastructure, and law enforcement. However, the tax burden in NYC can be significant, and many residents and businesses struggle to fully grasp the nuances of the system. This lack of understanding can lead to costly mistakes, missed deductions, or even penalties for non-compliance. As such, it's essential to stay informed and proactive when it comes to managing your tax obligations.

Throughout this article, we'll explore the various aspects of NYC state tax, including how it's calculated, who is subject to it, and how you can minimize your liability. We'll also address common misconceptions, share expert tips, and provide resources to help you stay ahead of the curve. Whether you're a newcomer to the city or a long-time resident, this guide will equip you with the knowledge and tools you need to make informed decisions about your finances. Let's get started by examining the basics of NYC state tax and its impact on everyday life.

Read also:Unveiling The Secrets Of Chttpswwwfacebookcom Your Ultimate Guide To Social Media Power

Table of Contents

- What Is NYC State Tax?

- How Does NYC State Tax Work?

- Who Pays NYC State Tax?

- How Much Is NYC State Tax?

- How Can I Reduce My NYC State Tax Liability?

- Why Is NYC State Tax So High?

- What Are the Penalties for Not Paying NYC State Tax?

- Frequently Asked Questions

- Conclusion

What Is NYC State Tax?

NYC state tax refers to the various forms of taxation imposed by the State of New York and the City of New York on individuals and businesses. This includes income tax, sales tax, property tax, and other specialized levies. While the federal government sets national tax policies, states and municipalities have the authority to establish their own tax systems to generate revenue for local needs. In New York City, these taxes play a critical role in funding public services, infrastructure projects, and community initiatives.

One of the most significant components of NYC state tax is the personal income tax, which applies to residents, non-residents who earn income in the city, and certain businesses. The tax rate varies depending on income levels, with higher earners paying a larger percentage of their income. Additionally, businesses operating in New York City are subject to corporate income tax, which is calculated based on their profits. These taxes are collected by the New York State Department of Taxation and Finance and the New York City Department of Finance.

Beyond income tax, residents and businesses also encounter sales tax, which is applied to most goods and services purchased within the city. Property owners must pay property tax, which is assessed based on the value of their real estate. Together, these taxes create a complex web of financial obligations that require careful planning and management. Understanding the scope and purpose of NYC state tax is the first step toward effective tax compliance and financial planning.

How Does NYC State Tax Work?

NYC state tax operates through a combination of state and local tax laws, each with its own set of rules and regulations. At the state level, the New York State Department of Taxation and Finance oversees the collection of income tax, sales tax, and other levies. Meanwhile, the New York City Department of Finance handles municipal taxes, including property tax and business taxes. This dual system ensures that both state and city governments receive the funding they need to operate efficiently.

For individuals, income tax is calculated based on their taxable income, which is determined by subtracting allowable deductions and exemptions from their gross income. The tax rate increases progressively, meaning that higher earners pay a larger percentage of their income. Employers are required to withhold state and city income taxes from employees' paychecks, which are then reconciled during the annual tax filing process. Self-employed individuals and freelancers must also pay estimated taxes quarterly to avoid penalties.

Businesses, on the other hand, are subject to corporate income tax, which is based on their net income after deductions. Certain industries, such as financial services and real estate, may face additional taxes or surcharges. Additionally, businesses must collect and remit sales tax on eligible transactions, ensuring that the correct amount is passed on to the appropriate tax authorities. The complexity of NYC state tax necessitates careful record-keeping and compliance to avoid costly mistakes.

Read also:Elizabeth Pitko The Rising Star In The World Of Entertainment

Why Is NYC State Tax Unique?

New York City's tax system stands out due to its combination of state and local taxes, which creates a higher overall tax burden compared to many other cities in the United States. For example, while the federal income tax rate ranges from 10% to 37%, New York State imposes an additional tax rate of up to 8.82%, and New York City adds another layer of taxation with rates ranging from 3.078% to 3.876%. This multi-tiered approach reflects the city's need to fund its extensive public services and infrastructure projects.

Another unique aspect of NYC state tax is the presence of specialized taxes, such as the Metropolitan Commuter Transportation Mobility Tax (MCTMT), which applies to businesses with a payroll exceeding $1 million. This tax helps support the city's transportation network, including the subway and bus systems. Similarly, the Commercial Rent Tax (CRT) imposes an additional levy on businesses leasing commercial space in certain parts of Manhattan. These specialized taxes highlight the city's focus on addressing specific economic and social challenges through targeted fiscal policies.

Who Pays NYC State Tax?

The scope of NYC state tax extends to a wide range of individuals and entities, including residents, non-residents, and businesses. Residents of New York City are required to pay both state and city income taxes, regardless of their employment status. This includes full-time employees, part-time workers, freelancers, and retirees who receive pension income. Non-residents who work in New York City are also subject to city income tax on the portion of their earnings attributable to their work in the city.

Businesses operating in New York City must pay corporate income tax, as well as other applicable taxes such as sales tax, property tax, and specialized levies. The tax obligations of a business depend on its structure, industry, and location. For instance, a small retail shop in Queens may only need to worry about sales tax and property tax, while a large financial services firm in Manhattan may face additional taxes related to its payroll and real estate holdings. Understanding these distinctions is essential for ensuring compliance and optimizing tax planning.

In addition to individuals and businesses, certain nonprofit organizations and trusts may also be subject to NYC state tax, depending on their activities and income sources. These entities must carefully review their tax obligations to avoid unexpected liabilities. The complexity of the tax code means that many taxpayers benefit from consulting with a tax professional or accountant to ensure they meet all their obligations and take advantage of available deductions and credits.

How Do Non-Residents Handle NYC State Tax?

Non-residents who work in New York City face unique challenges when it comes to NYC state tax. Since they only pay city income tax on the portion of their income earned in the city, accurately allocating their earnings is crucial. This often requires detailed record-keeping and coordination with their employers to ensure proper withholding. Non-residents must also be aware of potential double taxation issues, as they may owe state income tax to their home state as well as New York City. To mitigate this risk, they should explore available credits or agreements between states that may reduce their overall tax burden.

How Much Is NYC State Tax?

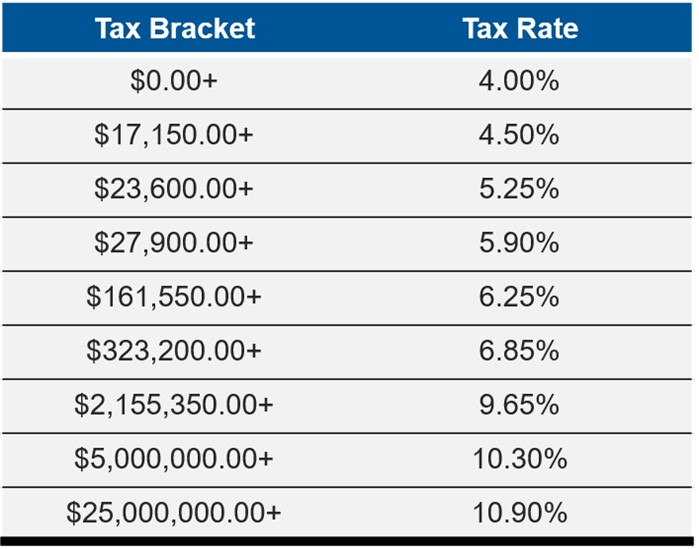

The amount of NYC state tax owed depends on several factors, including income level, tax filing status, and the type of tax being assessed. For personal income tax, the combined state and city tax rates range from approximately 6.09% to 12.696% for the highest earners. This progressive tax structure ensures that those with higher incomes contribute a larger share of their earnings to support public services and infrastructure. Additionally, certain taxpayers may qualify for deductions and credits that reduce their taxable income, lowering their overall tax liability.

Sales tax in New York City is currently set at 8.875%, which includes the state rate of 4%, the city rate of 4.456%, and a Metropolitan Commuter Transportation District surcharge of 0.4%. This tax applies to most goods and services purchased within the city, although some items, such as food and clothing under $110, are exempt. Property tax rates vary depending on the type of property and its assessed value, with residential properties generally facing lower rates than commercial properties.

Businesses must calculate their corporate income tax based on their net income after deductions, with rates ranging from 6.5% to 8.85%. Certain industries, such as financial services and real estate, may face additional taxes or surcharges. Overall, the complexity of NYC state tax means that taxpayers must carefully review their financial situation to determine their exact liability and explore opportunities to minimize their burden.

What Are the Deductions and Credits Available?

To help taxpayers reduce their NYC state tax liability, the state and city offer a variety of deductions and credits. For individuals, common deductions include contributions to retirement accounts, mortgage interest, and charitable donations. Credits may be available for dependents, education expenses, and energy-efficient home improvements. Businesses can also take advantage of deductions for business expenses, depreciation, and research and development activities. Understanding these deductions and credits is essential for maximizing tax savings and ensuring compliance.

How Can I Reduce My NYC State Tax Liability?

Reducing your NYC state tax liability requires a combination of strategic planning and careful execution. Start by taking full advantage of available deductions and credits, which can significantly lower your taxable income. For example, contributing to a retirement account not only helps you save for the future but also reduces your current tax burden. Similarly, investing in energy-efficient home improvements can qualify you for valuable tax credits.

For businesses, effective tax planning involves careful expense management, strategic timing of transactions, and leveraging available incentives. This may include deferring income to a future tax year, accelerating deductible expenses, or restructuring your business to take advantage of favorable tax treatments. Consulting with a tax professional or accountant can provide valuable insights and ensure that you're maximizing your savings while staying compliant with the law.

In addition to these strategies, consider exploring opportunities for tax deferral or abatement. For example, certain real estate developments may qualify for tax abatements that reduce property tax liability for a specified period. Similarly, businesses investing in renewable energy projects may benefit from federal and state tax incentives. By staying informed about these opportunities and acting proactively, you can significantly reduce your NYC state tax liability and improve your financial well-being.

What Are the Best Practices for Tax Planning?

Effective tax planning involves a proactive approach to managing your financial affairs throughout the year, rather than waiting until tax season. Start by keeping detailed records of your income, expenses, and deductions, using software or apps to streamline the process. Regularly review your financial situation to identify potential tax-saving opportunities and address any issues before they become major problems. Additionally, stay informed about changes in tax laws and regulations that may affect your liability, and adjust your strategies accordingly.

Why Is NYC State Tax So High?

The high level of NYC state tax reflects the city's need to fund its extensive public services and infrastructure projects. New York City is home to a vast network of public transportation, world-class educational institutions, and state-of-the-art healthcare facilities, all of which require significant financial resources to maintain and improve. Additionally, the city faces unique challenges such as rising housing costs, environmental concerns, and social inequality, which necessitate targeted fiscal policies to address these issues.

Another factor contributing to the high tax burden is the city's large population and diverse economy. With millions of residents and businesses generating billions in economic activity, New York City requires a robust tax system to support its operations. While some critics argue that the high tax rates discourage investment and migration, proponents point to the city's strong economic performance and quality of life as evidence of the system's effectiveness.

Ultimately, the level of NYC state tax reflects a balancing act between generating sufficient revenue to